The REWIRE Act Would Fast-Track Transmission Upgrades. Here's What That Means for Equipment Demand.

Bipartisan legislation creates a NEPA categorical exclusion for reconductoring within existing rights-of-way, potentially unlocking $85 billion in grid cost savings by 2035. The procurement implications are significant.

U.S. electricity demand is projected to rise as much as 5.7% by 2030. That’s the fastest growth rate since the 1960s, following two decades where load was essentially flat. The infrastructure was not built for this, and new greenfield transmission takes 10 to 15 years to permit.

The REWIRE Act, introduced March 2 by Senators Dave McCormick (R-PA) and Peter Welch (D-VT), is a bipartisan attempt to address the bottleneck. Senate Bill 3947 creates a NEPA categorical exclusion for projects that increase grid capacity within existing rights-of-way. That includes reconductoring with advanced conductors, deploying grid-enhancing technologies, and co-locating energy storage. The bill has support from more than 35 organizations, including NEMA, the American Clean Power Association, PPL Corporation, and EQT.

The legislation targets a specific problem: new transmission lines are slow to build, but upgrading existing lines is fast. And the equipment required for each path is very different.

What the Bill Actually Does

Three provisions matter for equipment procurement:

NEPA categorical exclusion for reconductoring. This is the headline. Projects that upgrade conductors within existing rights-of-way wouldn’t require environmental assessments. For utilities that have been sitting on reconductoring plans because of permitting uncertainty, this removes the single largest procedural barrier. The timeline compression is significant: years of environmental review reduced to months.

FERC return-on-equity incentive. Within one year of enactment, FERC must revise its ROE rules to incentivize investment in advanced transmission conductors. This directly improves the financial case for utilities to replace conventional ACSR conductors with higher-capacity alternatives. Regulated utilities respond to ROE signals. This one points toward reconductoring.

DOE national clearinghouse. The Department of Energy would create a centralized database of advanced transmission technology applications, case studies, and best practices. Through the National Labs and in consultation with FERC and NERC, DOE would also develop probabilistic grid planning models that account for weather, congestion, and technology costs. The clearinghouse gives smaller utilities and cooperatives access to deployment data they would not otherwise have.

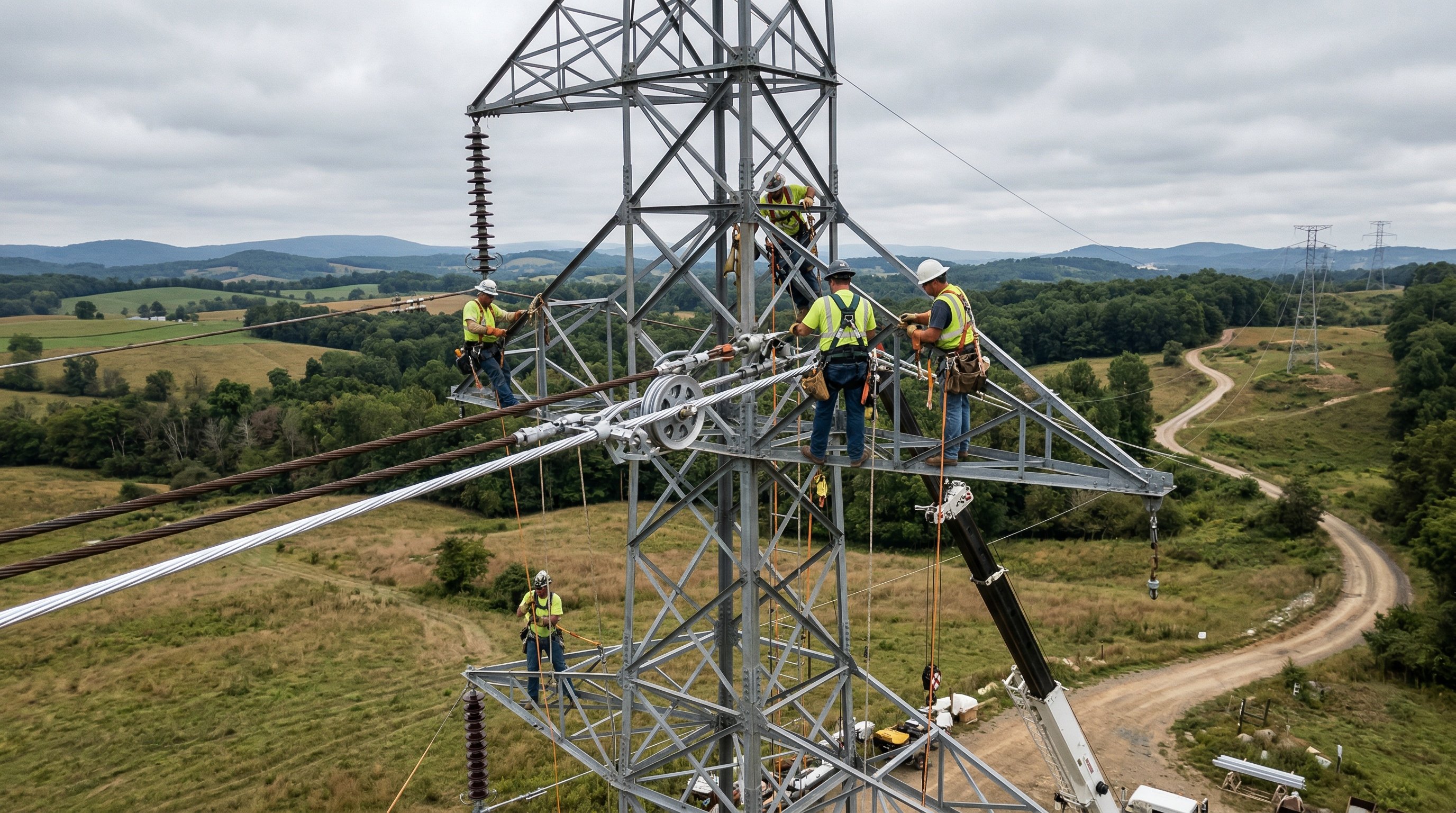

The Equipment This Legislation Pulls Forward

Advanced conductors are the primary category. The reconductoring pathway replaces conventional aluminum conductor steel-reinforced (ACSR) lines with advanced composite core conductors or high-temperature low-sag (HTLS) conductors that can carry roughly double the power on the same towers. The active manufacturers in this space include CTC Global (ACCC), TS Conductor (AECC), and Southwire (C7 and ACSS). Each uses a different composite core design, but the end result is similar: higher capacity and lower sag on existing structures.

Worth noting for procurement teams: these manufacturers have very different domestic manufacturing footprints. TS Conductor and Southwire are vertically integrated in the U.S., manufacturing the finished conductor domestically. CTC Global manufactures its carbon fiber cores in California but relies on a network of licensed third-party strandors to produce the finished conductor, which creates a more distributed supply chain. For projects that involve federal funding, the distinction matters. (More on that below.)

Grid-enhancing technologies (GETs) are the second category. The bill’s categorical exclusion also covers dynamic line ratings, power flow controllers, and topology optimization. These are lower-cost interventions that can be deployed in months rather than years. They serve as both a complement to reconductoring and a standalone capacity solution.

The third category is less obvious but significant for distributors: substation equipment. Doubling the capacity of a transmission line means the substations at both ends need to handle the increased power flow. Termination hardware, disconnect switches, and in some cases transformer upgrades are required wherever reconductored lines connect to the rest of the grid. This creates distribution-side equipment demand from legislation that is nominally about transmission.

Why This Bill Has Political Legs

Grid legislation has a track record of dying in partisan fights over clean energy policy. The REWIRE Act avoids that framing entirely. The pitch is infrastructure maintenance and cost reduction, not decarbonization. Reconductoring using existing rights-of-way is a concept that resonates on both sides of the aisle: it’s faster, cheaper, and less disruptive than building new transmission.

The bipartisan sponsorship (a Pennsylvania Republican and a Vermont Democrat) and the breadth of the coalition (35+ organizations from fossil energy, clean energy, and utility sectors) suggest this is not a messaging bill. The $85 billion in projected cost savings by 2035 and $180 billion by 2050 give fiscal hawks a reason to support it.

Whether it passes this session is uncertain. What is not uncertain is the policy direction. Every major grid proposal in the 119th Congress, including the DOE SPARK program’s $1.9 billion in grid resilience funding, points toward accelerating capacity expansion on existing infrastructure. And where federal dollars flow, Buy America requirements follow.

What This Means for Procurement Teams

For distributors and procurement professionals watching the legislative calendar, the REWIRE Act signals where federal policy is heading even if the specific bill stalls.

The demand drivers are already in place. Transformer lead times remain stretched, with large power units at 128 weeks as of Wood Mackenzie’s most recent survey. T&D infrastructure spending is accelerating across every major IOU, with distribution costs at some utilities up more than 100% since 2020. Data center interconnection requests have pushed MISO to 43% annual load growth, and projects like the $33 billion Ohio power build are adding multi-gigawatt loads to regional grids.

The REWIRE Act doesn’t create demand. The demand already exists. What the legislation does is compress the timeline for a specific category of response: upgrading existing transmission lines rather than waiting a decade for new ones. For procurement teams, that means the advanced conductor and GET categories move from future consideration to near-term purchasing decisions faster than many capital plans currently assume.

The Buy America Factor

The REWIRE Act itself does not include Buy America provisions. But many of the projects it would accelerate will tap federal funding, including programs like the DOE SPARK initiative and other IIJA-funded grid investments, where Build America Buy America (BABA) requirements already apply. Under BABA, manufactured products used in federally funded infrastructure must be assembled in the U.S. with greater than 55% domestic component cost.

This matters for advanced conductor procurement. Not all manufacturers are equally positioned. Southwire and TS Conductor operate vertically integrated U.S. manufacturing, from raw materials through finished conductor under domestic roofs. CTC Global’s model is different: cores are made in California, but the finished ACCC conductor is stranded by licensed third parties across a global network. Whether a given CTC-sourced conductor meets BABA’s domestic content threshold depends on who strands it and where the aluminum is sourced.

Procurement teams evaluating advanced conductors for federally funded projects should be asking suppliers directly about BABA compliance documentation for the finished product, not just where the core is manufactured. The distinction between “made in America” as a marketing claim and BABA compliance as a legal standard is real, and it narrows the field of qualified suppliers more than most equipment catalogs suggest.

Distributors who serve utilities with aging transmission infrastructure and growing load pressures should be tracking this bill. If it passes, the orders for advanced conductors, HTLS, DLR sensors, and associated substation hardware will accelerate. If it does not pass, the underlying demand signals remain, and the equipment categories it highlights are relevant regardless.

The Grid Brief delivers weekly procurement intelligence on grid infrastructure developments like this. Subscribe here.

Frequently Asked Questions

What is the REWIRE Act?

The Reconductoring Existing Wires for Infrastructure Reliability and Expansion (REWIRE) Act (S.3947) is bipartisan legislation introduced by Senators McCormick (R-PA) and Welch (D-VT) that creates a NEPA categorical exclusion for projects that increase grid capacity within existing rights-of-way, including reconductoring with advanced conductors and deploying grid-enhancing technologies.

How does the REWIRE Act affect equipment procurement?

The bill would accelerate demand for advanced composite core conductors, high-temperature low-sag (HTLS) conductors, and associated hardware from manufacturers like CTC Global, TS Conductor, and Southwire. It also drives demand for grid-enhancing technologies like dynamic line rating sensors and power flow controllers. Substation upgrades at line terminations create additional distribution-side equipment demand.

Do Buy America requirements apply to REWIRE Act projects?

The REWIRE Act itself does not include Buy America provisions. However, many reconductoring projects will use federal funding from programs like DOE SPARK where Build America Buy America (BABA) requirements already apply under existing law. BABA requires manufactured products to be assembled in the U.S. with greater than 55% domestic component cost, which narrows the field of qualified advanced conductor suppliers.

What is reconductoring and why does it matter?

Reconductoring replaces existing transmission line conductors with advanced conductors that can carry roughly double the power on the same towers and rights-of-way. It matters because new greenfield transmission projects face 10-15 year permitting timelines, while reconductoring can be completed in months to a few years using existing infrastructure.

How much could the REWIRE Act save in grid costs?

Estimates suggest reconductoring at scale could reduce grid costs by $85 billion by 2035 and $180 billion by 2050 by reducing transmission congestion and avoiding the lengthy permitting process required for new transmission lines.

Municipal Procurement Tracker — Q2 2026

Active bid opportunities, award trends, and procurement patterns across U.S. municipal utilities. Use it to time your outreach.

The Grid Brief

Lead times. Pricing shifts. Funding deadlines. Delivered Thursday mornings.